The amount of interest reduces the amount of cash that the borrower receives up front. Note Payable is credited for the principal amount that must be repaid at the end of the term of the loan. For this illustration, let’s make a journal entry for the first installment. Below is the portion of the amortization schedule for your convenience.

- To accomplish this process, the Discount on Notes Payable account is written off over the life of the note.

- Interest is now included as part of thepayment terms at an annual rate of 10%.

- An interest-bearing note is a promissory note with a stated interest rate on its face.

- Finally, at the end of the 3 month term the notes payable have to be paid together with the accrued interest, and the following journal completes the transaction.

- The terms of the agreement will state this resale possibility, and the new debt owner honors the agreement terms of the original parties.

Accounting Ratios

Debt sale to a third party is a possibility with any loan, which includes a short-term note payable. The terms of the agreement will state this resale possibility, and the new debt owner honors the agreement terms of the original parties. A lender may choose this option to collect cash quickly and reduce the overall outstanding debt. There is an ebb and flow to business that can sometimes produce this same situation, where business expenses temporarily exceed revenues. Even if a company finds itself in this situation, bills still need to be paid.

Short-Term Note Payable – Discounted

This establishes the importance of notes payable recording in financial statements. Under the accrual accounting system, the company records its outstanding liabilities and receivables irrespective of when a cash payment is made. The accrued transactions give rise to different assets and liabilities in the balance sheet of the company.

The Journal Entry For Payment Of Loan On The Due Date

The due date and allowed period are also mentioned on the note payable. The time allowed for payment is an agreed-upon timeline at the will of both parties to contracts. It can be three months, six months, one year, or as the parties consider feasible. A note payable might be written if the debtor has failed to pay the promised amount on the due date. The account payable might be converted into a note payable on non-payment beyond the due date. Notes payable are most generally issued by the borrower or the lender when a bank loan is taken.

What is the approximate value of your cash savings and other investments?

Textbook content produced by OpenStax is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike License . To simplify the math, we will assume every month has 30 days and each year has 360 days. In examining this illustration, one might wonder about the order in which specific current obligations are to be listed. One scheme learn bookkeping and accounting online for free is to list them according to their due dates, from the earliest to the latest. Another acceptable alternative is to list them by maturity value, from the largest to the smallest. Our writing and editorial staff are a team of experts holding advanced financial designations and have written for most major financial media publications.

Notes payable vs. accounts payable

The organization borrows money from the owner of the firm, and the borrower agrees to repay the amount borrowed plus interest at a specified date in the future. In this case the note payable is issued to replace an amount due to a supplier currently shown as accounts payable, so no cash is involved. The company obtains a loan of $100,000 against a note with a face value of $102,250. The difference between the face value of the note and the loan obtained against it is debited to discount on notes payable. The note payable issued on November 1, 2018 matures on February 1, 2019. On this date, National Company must record the following journal entry for the payment of principal amount (i.e., $100,000) plus interest thereon (i.e., $1,000 + $500).

One thing to be noted for the notes payable is that the interest payable or interest liability has not been recorded in the first entry. It’s because the interest amount was not due on the date of loan issuance. An interest-bearing note payable may also be issued on account rather than for cash. In this case, a company already owed for a product or service it previously was invoiced for on account.

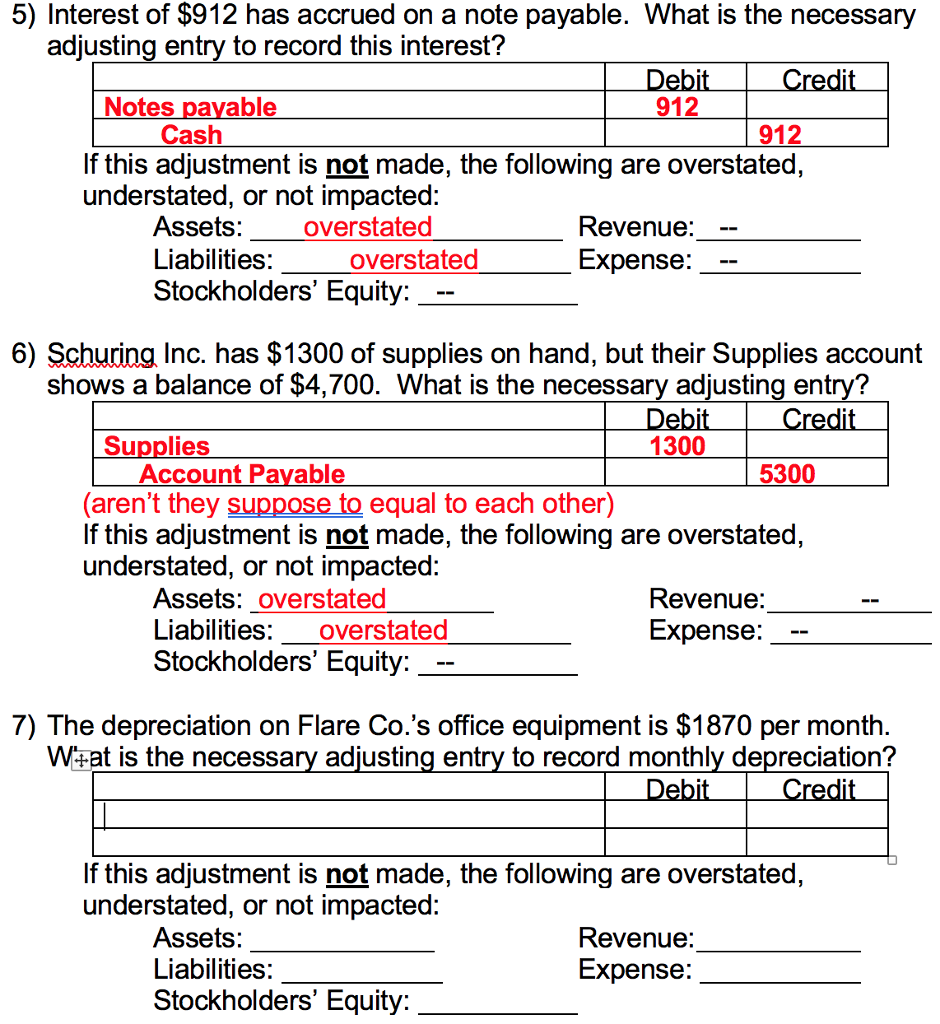

Notes payable on the balance sheet take a spot under the liabilities column. They are considered current liabilities when the amount is due within one year, and else they are recorded under the long-term liabilities category. If the company does not make this journal entry, both total expenses on the income statement and total liabilities on the balance sheet will be understated by $2,500 as of December 31, 2020.

With accounts payable, the amount paid for each item might change due to frequency of use. For example, accounts payable could include charges for things like utilities and legal services, rather than bank loans. Short-term debt may be preferred over long-term debt when theentity does not want to devote resources to pay interest over anextended period of time. In many cases, the interest rate is lowerthan long-term debt, because the loan is considered less risky withthe shorter payback period. This shorter payback period is alsobeneficial with amortization expenses; short-term debt typicallydoes not amortize, unlike long-term debt. You create the note payable and agree to make payments each month along with $100 interest.

You can see the kind of information that is added to the note payable. The company owes $10,999 after this payment, which is $21,474 – $10,475. The company owes $21,474 after this payment, which is $31,450 – $9,976.

The notes payable is an agreement that is made in the form of the written notes with a stronger legal claim to assets than accounts payable. The company usually issue notes payable to meet short-term financing needs. Whether or not the note is classified as a current or long-term liability will depend on its due date.